The Altagamma-Bain Worldwide Luxury Market Monitor and the trends in the luxury goods sector

The 20th Altagamma Observatory, presented in Milan in November 2021, reports a consumption recovery in all luxury sectors; at the same time, the events of the last two years have accelerated ongoing changes that we will see in the coming years.

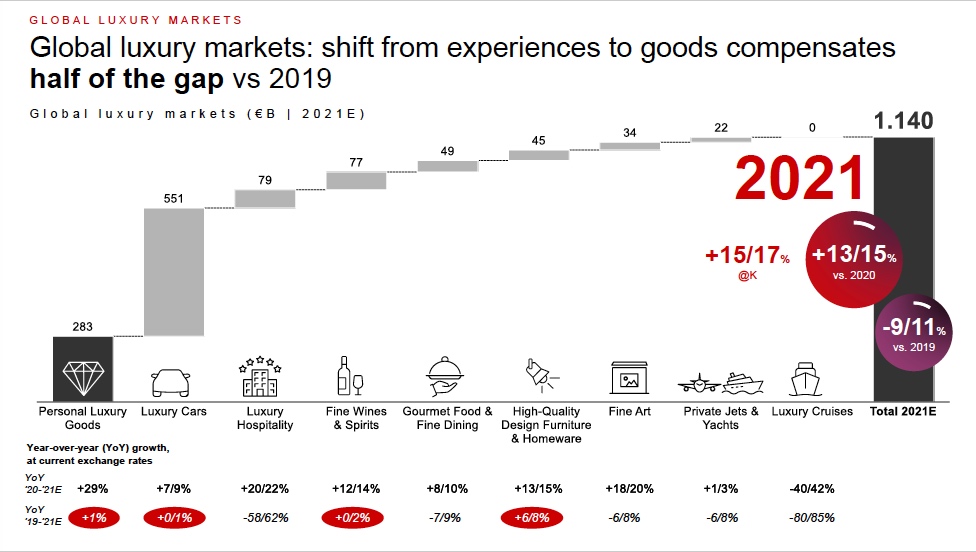

The Altagamma-Bain Worldwide Luxury Market Monitor 2021 estimates growth in the global luxury goods sector at €1,140 billion, recovering about half of the 2020 losses. For personal luxury goods, there is a full recovery, with a 2021 market value forecast of € 283 billion, +1% from 2019.

According to the Altagamma-Bain Worldwide Luxury Market Monitor 2021, the overall luxury market, which includes both luxury goods and experiential goods, is showing a substantial recovery in 2021 over 2020. The global value of the market is approximately 1.1 trillion euros. The most relevant finding from the analysis is that the pandemic has caused a marked shift in spending from experiences to goods, particularly furniture, design, food and fine wines.

Read also Selling furniture online after the pandemic

Furniture and design are still growing

Designer and high-end furniture have grown 13/15% over 2020, and 6/8% between 2019 and 2021. The forced presence at home in 2020 gave back to the house a new central role; spaces increasingly mix living and working functions, giving rise to new product categories. The core market of high-end design, which showed a stronger-than-forecasted performance in the last quarters of 2020, continues its growth. In fact, consumers’ focus on the home is stable, particularly on living, bedroom, outdoor and lighting. Moreover, the interpenetration of living and working spaces also fuels the search for comfort, functionality and flexibility in design solutions.

However, consumers’ desire to resume experiences is at an all-time high, with their recovery primarily dependent on the normalization of travel.

China and North America lead the recovery

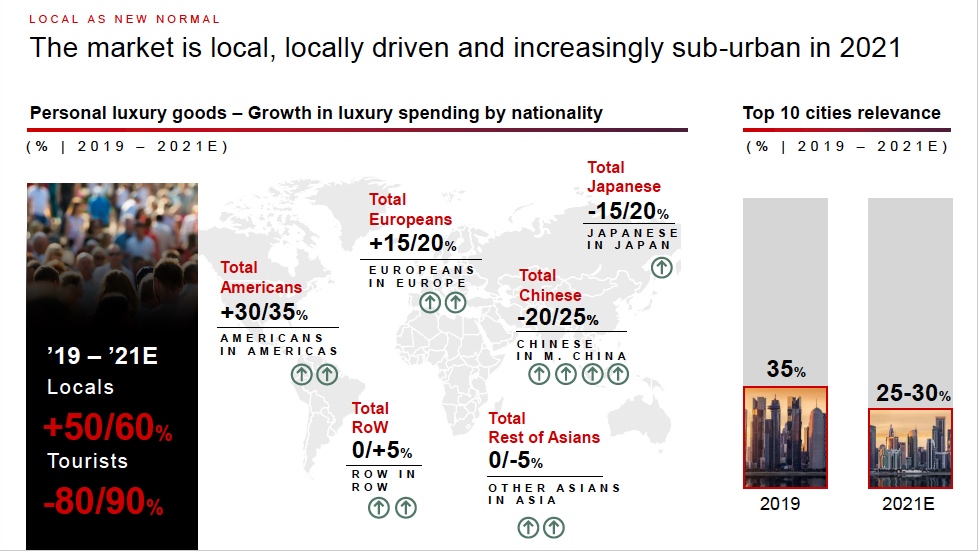

In geographic terms, mainland China has led the recovery, doubling its market compared to 2019. There has also been a solid recovery in the United States (already above 2019 levels). The Americas have now become the world’s largest market for luxury, representing 31% of the global market, the Middle East was another fast-growing market (above 2019 levels and + 34% compared to 2020). Europe (+20% compared to 2020), Japan (+10%) and the rest of Asia (+19%), on the other hand, have only partially recovered during 2021 and have not yet reached pre-Covid levels.

As for product categories, the footwear market reached 23 billion euros in 2021 (+11% compared to 2019). Bags have brought in 62 billion euros this year, +8% compared to 2019. In 2021 Jewelry grew by 7% compared to 2019, at 23 billion euros. Lastly, while watches, cosmetics and fragrances have returned to 2019 levels, clothing has yet to recover (-10% compared to 2019).

The market has been supported by the recovery in local consumption, the combined effect of China and the United States, and the continued strength of the online channel. Younger customers (Gen Y and Gen Z) continue to drive growth and together they will make up 70% of the market by 2025.

What future for luxury goods?

Therefore, 2021 could be considered a “year zero” for consumption, the beginning of a new cycle that will see consumers change significantly in a few years as Gen Y and Z become the main customers. China and America will always lead the market, with numerous offshoots in other places, some of which have probably yet to emerge. New consumers will be more interested in the product and less in the brand; environmental awareness will drive the second-hand luxury market.

Discover Deesup, the marketplace for second-hand design furniture

The pandemic has caused changes in the market that could be permanent. In fact, it is estimated that a segment of the older generation may have left the luxury goods market permanently, and by 2025 some balances will be permanently altered. In addition to demographic changes, sales and distribution channels will play a crucial role; online sales doubled in volume between 2019 and 2021. Online sales pose a question of new paradigms; the focus is on the awareness phase, which will be increasingly important for brand recognition. New consumers will be increasingly attentive to the values a brand expresses and less and less to appearance/icon, and even less to price range. Moreover, they will be increasingly sensitive to sustainability.